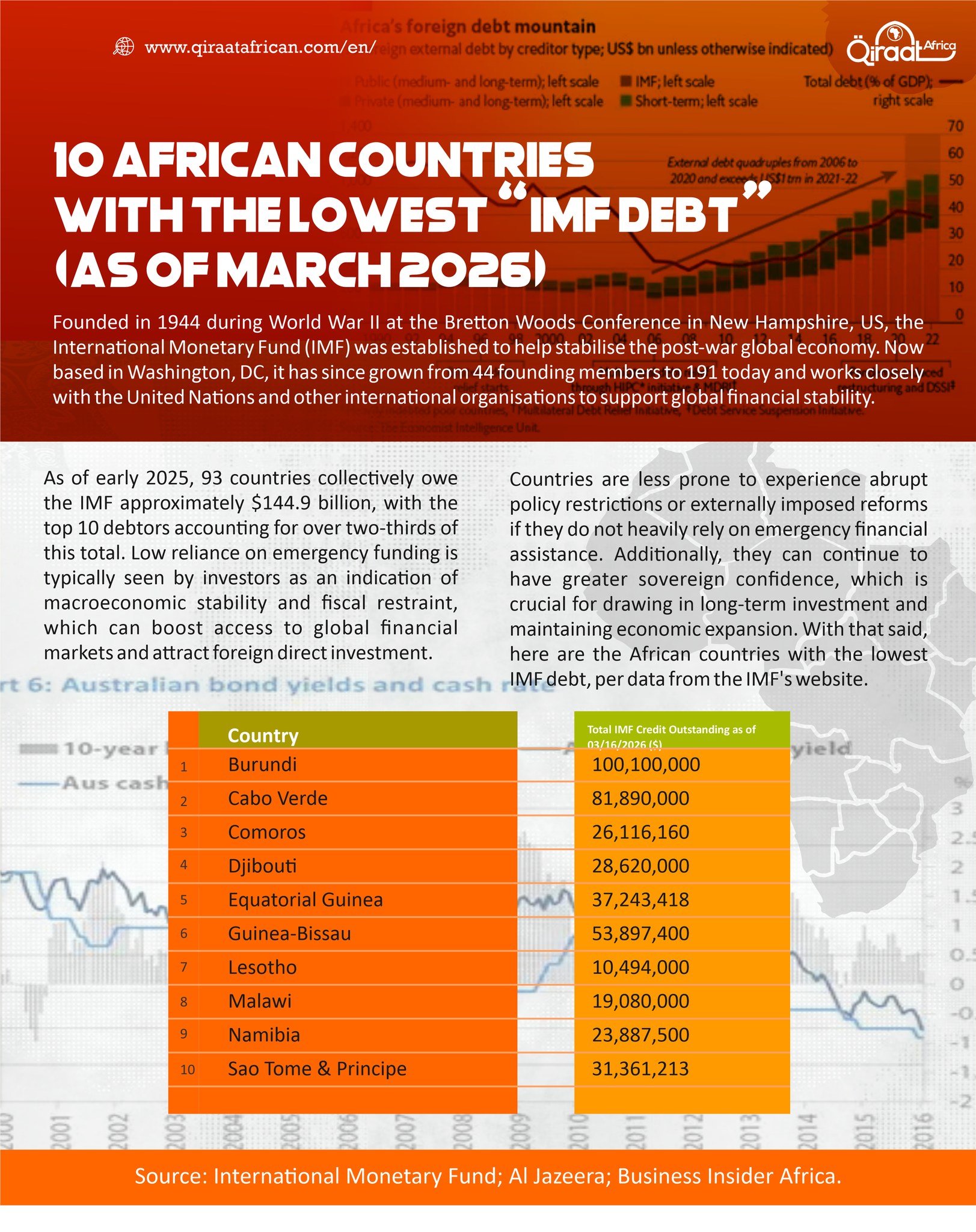

Founded in 1944 during World War II at the Bretton Woods Conference in New Hampshire, US, the International Monetary Fund (IMF) was established to help stabilise the post-war global economy. Now based in Washington, DC, it has since grown from 44 founding members to 191 today and works closely with the United Nations and other international organisations to support global financial stability.

As of early 2025, 93 countries collectively owe the IMF approximately $144.9 billion, with the top 10 debtors accounting for over two-thirds of this total. Low reliance on emergency funding is typically seen by investors as an indication of macroeconomic stability and fiscal restraint, which can boost access to global financial markets and attract foreign direct investment.

Countries are less prone to experience abrupt policy restrictions or externally imposed reforms if they do not heavily rely on emergency financial assistance. Additionally, they can continue to have greater sovereign confidence, which is crucial for drawing in long-term investment and maintaining economic expansion. With that said, here are the African countries with the lowest IMF debt, per data from the IMF’s website.

{kind=link}