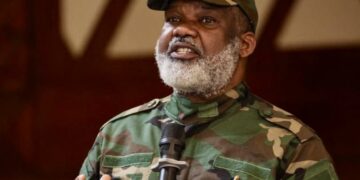

Barely a few weeks after his inauguration, media reports reveal that the ambitious moves of Nigeria’s new president, Bola Ahmed Tinubu, have been shaking Nigeria to its very core, aiming at restructuring the country’s financial sector in an absolutely mind-boggling sequence of events. Tinubu has “descended upon Nigeria like a typhoon”, exercising tough decisions most times. Although Nigerians strongly supported him in the election despite his alleged “dubious” moral character and infamous political power, most Nigerians know that he may not wholly clean up corruption or fight the cabal. However, Nigerians have faith and are full of expectations regarding his moves to restore economic stability.

President Bola Ahmed Tinubu was inaugurated on May 29, 2023, with the ceremony taking place amid tight security at the 5,000-capacity Eagle Square venue in the capital, Abuja. Albeit, media reports reveal that he will be facing a “fractured nation, an ailing economy, and spiralling insecurity.” However, despite Nigerians finding themselves amidst a mixture of anticipation and unease, President Tinubu’s political influence proved to be the driving force behind his victory and most of his actions now. Hence, the expectations of Nigerians regarding him seem to lie primarily in the realm of economic stability rather than others.

President Tinubu inherits an economy riddled with huge debt from his predecessor, Buhari, according to economic experts. But President Bola Tinubu, during his inauguration, vowed and reinstated that he would expand the economy by “at least six percent a year, lift barriers to investment, create jobs, and unify the exchange rate while also tackling rampant insecurity.”

“On the economy, we target higher GDP [gross domestic product] growth and to significantly reduce unemployment.” He continued, “I have a message for our investors, local and foreign: our government shall review all their complaints about multiple taxes and various anti-investment inhibitions.”

In terms of reforms, the administration appears to have made significant progress in a short period of time; however, what is conspicuously lacking are actions that directly affect the populace. For example, the effects of subsidy removal on the masses are still ongoing, even though his administration directed that palliatives be put in place to soften the effect of the removal of petrol subsidies on the masses.

Fuel subsidy saga

Tinubu’s first day in office, just after taking the oath of office, was greeted with some criticism and surprise. He promptly reviewed the contentious topic of subsidy and announced its removal from Premium Motor Spirit (PMS), more commonly known as gasoline. For obvious reasons, many Nigerians appear not to be on the same page with the development.

The statement had unexpected results for the masses and the economy immediately. Petroleum product marketers quickly increased the price of gasoline to N540 per litre. Hence, some Nigerians who cannot afford to pay the new charges parked their vehicles at home and preferred boarding motorists, while some masses, below average, resorted to walking long distances in communities or rather paying exorbitant prices. The masses continue to endure the worst of it as a new reality and carry on as normal, despite the decision appearing tough.

The president, with his motive, had earlier said, “Subsidy can no longer justify its ever-increasing costs in the wake of drying resources. We shall instead re-channel the funds into better investment in public infrastructure, education, healthcare, and jobs that will materially improve the lives of millions.”

Masses are still hanging on and expecting the promises to be fulfilled, as “the petrol subsidy removal has been anticipated to cause a temporary increase in inflation in the upcoming months before contributing to disinflation in the medium term.”

Decisions on tax and foreign investments

President Tinubu’s administration has outlined a plan of action aimed at producing greater GDP growth, which would in turn promote a major reduction in unemployment. His major goal is to reconstruct the economy to bring about growth and development through the creation of jobs, food security, and an end to extreme poverty.

According to some economic analysts, the President “intends to accomplish this through budgetary reform to stimulate the economy without engendering inflation and industrial policy to utilise the full range of fiscal measures to promote domestic manufacturing and lessen import dependency.”

Research also shows that President Tinubu’s administration “has also touched on the monetary policy reforms, which led to the Central Bank of Nigeria (CBN) discarding the multiple foreign exchange FX rates it had hitherto maintained in favour of a unified exchange rate. The aim is to divert funds from arbitrage into meaningful investment in the plants, equipment, and jobs that power the real economy. This is in addition to allowing the redesigned Naira and the old denominations to run both as legal tender.”

Nigerian Special Adviser to the President on Special Duties, Communication, and Strategy, Mr. Dele Alake, disclosed in a press briefing at the Presidential Villa, Abuja, that President Tinubu signed four Executive Orders “in fidelity to the pledge to put Nigerians at the centre of government policies and address business-unfriendly fiscal policy measures and multiplicity of taxes”.

They are the Finance Act (Effective Date Variation) Order, 2023; The Customs, Excise Tariff (Variation) Amendment Order, 2023; an order suspending the 5% Excise Tax on telecommunication; and the suspension of the newly introduced Green Tax by way of the Excise Tax on Single-Use Plastics. These orders also came with adjustments in other areas, like the suspension of the Import Tax Adjustment levy on vehicles.

These moves are all in a bid to generate revenue or adjust levies, either at the Federal level or at the state level. One of the commendable steps President Tinubu’s administration took to generate regional or state-level resources was assenting to the Electricity Bill 2023. The Bill makes room for electricity to be more accessible and inexpensive for businesses and homes alike, as it allows subnationals to generate their own electricity. It was also done in an effort to nearly double power generation and enhance the transmission and distribution networks as states establish their own regional resources.

However, another economic policy of President Tinubu’s administration that does not go well with some Nigerians is the recent imposition of a yearly car ownership verification tax of N1,000 for all categories of motorists across the nation. The National Vehicle and Identification Scheme (NVIS) database keeps track of the status and integrity of every vehicle registered there, according to the government, which argues that is what the fee known as the Proof of Ownership Certificate (POC) is intended to do.

“Renewed Hope”

Just like Bola Ahmed Tinubu’s campaign mantra before emerging as president, “Renewed Hope”, some political analysts and economic experts believe that Nigeria is on the path to greatness. But the question is, how long will the masses wait to endure policies’ results before things take shape positively?

Experts are unanimous in their views “that the various economic policies of President Tinubu are critical steps to address long-standing macroeconomic imbalances and have the potential to establish a solid foundation for sustainable and inclusive growth. They affirmed that Nigeria can seize this window of opportunity to further implement a comprehensive reform that encompasses a range of complementary fiscal, monetary, trade, and structural policy measures to maximise growth, job creation, and poverty reduction.”

Thus, they have applauded some of President Tinubu’s economic initiatives that have been made official so far and have also offered recommendations for the years to come. However, Nigerians are patiently waiting for the much-anticipated economic recovery that will bring about inclusive growth and a higher standard of living for all.

{kind=link}