Since the financial crisis in 2008, several initiatives to reform economic governance have been put forward in response to demands from governments, notably but not only ‘green growth’, ‘decarbonization’, and ‘green’, ‘blue’, or ‘circular’ economies. Over the past decade, the concept of the green economy has emerged as a strategic priority for many governments and intergovernmental organizations. All told, 65 countries have embarked on a path towards an inclusive green economy and related strategies. By transforming their economies into drivers of sustainability, they will be primed to take on the major challenges of the twenty-first century, from urbanization and resource scarcity to climate change and economic volatility. Some pathways to net-zero emissions assume that the decline in emissions begins immediately and progresses gradually to 2050, with appropriate measures in place to manage disruptions and limit costs. Others assume that the reduction of emissions begins later and progresses more quickly to achieve the same goal. The latter could involve significant and abrupt changes in policy, high carbon prices, and sudden changes to investment practices, along with greater socioeconomic effects and a larger-scale response.

The transition to a green economy is not hitch-free, as it involves certain risks and costs that always accompany such a paradigm shift. For instance, a green economy will require outright changes in the production processes in developing economies from the use of non-renewable and environmentally unfriendly resources to more sustainable ones, say replacing fossil fuels with renewable energy in power generation. Unfortunately, these economies have comparative disadvantages in terms of technical and human capital in the sectors that promote sustainable development. There are also other concerns about the likely tradeoff between national development plans and industrialization programs, the tenets of the green economy, the effects on tense North-South trade and policies, global inequality, and several other issues. Also, the most noticeable impacts on everyday lives will include rising energy bills, job losses in high-emission industries, changes in what people eat, and increasing outgoings to end our dependence on fossil fuels to heat homes and travel, the report says. Despite the COVID-19 impacts, renewable energy financing and investments are in a virtuous cycle of falling costs, expanding deployment, and accelerating technological progress. Solar panel equipment prices, for example, have fallen by about 80 percent since 2010, while wind turbine prices have fallen by 30 to 40 percent in the same period (see IREA). At the same time, a mismatch in the supply and demand for critical minerals for key clean energy technologies—cobalt, lithium, nickel, and copper—presents a business case for Africa’s engagement. The demand for lithium is expected to grow over 30 times by 2040, but supply from existing mines and projects under construction can only meet about half the projected demand.

‘Capturing the opportunity’ from Developing Countries

During the Cold War, developing nations were called ‘’the South,’’ which highlighted the great disparities between the industrially developed states in temperate climates (the North) and the less-developed states in tropical and semitropical zones (the South). According to a view known as neo-colonialism, the rich nations of the North continued to exploit the poor nations of the South even after the latter gained independence in the post-World War II period (see Understanding Politics: Ideas, Institutions, and Issues by Thomas M. Magstadt, p. . 264). While examining the economic gap between the North and the South, in the book published by Wadsworth titled Global Politics, Juliet Kaarbo and James Lee Ray, on page 390, stated that poverty, starvation, and glaring inequality in the distribution of the world’s wealth constitute a serious problem in many respects. Millions suffer grievously from poverty, and they probably will continue to do so for a long time to come.

Nevertheless, many analysts feel that the oil glut brought about a false sense of security. Indications are that the demand for energy will increase dramatically in the coming decades, spurred in part by economic growth in China and India (see Global Politics by Juliet Kaarbo and James Lee Ray, p. . 468). Experts said, ‘‘The decoupling of global electricity demand and emissions would be significant given the energy sector’s increasing electrification, with more consumers using technologies such as electric vehicles and heat pumps.” In fact, clean electricity accounted for around 80% of new capacity additions to the world’s electricity system in 2023, and electric vehicles accounted for around one out of five cars sold globally. At the same time, global investment in clean energy manufacturing is booming, driven by industrial policies and market demand. Employment in clean energy jobs exceeded that of fossil fuels in 2021 and continues to grow. However, the green recovery poses a particular challenge for developing countries rich in non-renewable resources, notably fossil fuels and minerals. For fossil fuel-exporting countries, low demand for fuel sources, in combination with policy pressure to reduce GHG emissions, would increase the urgency to diversify exports away from fossil fuels toward cleaner energy forms. For mineral-rich developing countries, the abatement of emissions from this sector could contribute significantly to overall emissions reductions. To achieve such objectives, countries rich in non-renewable resources will need to develop targeted policies in areas including fiscal and tax policy, financial, energy, and mining sector regulation, and low-carbon technology, while keeping a strong focus on equity aspects of the transition.

The broader vision of a thriving global green economy that our taxonomy enables implies decoupling economic activity from negative environmental impacts. Achieving this vision will place the global economy on a more sustainable path. That means averting the highly damaging impacts of global warming—not just on the environment but on economic prosperity too. Consulting firm McKinsey says total global spending by governments, businesses, and individuals on energy and land-use systems will need to rise by $3.5 trillion a year, every year, if we are to have any chance of getting to net-zero in 2050. Spending would be front-loaded—the next decade will be decisive—and the impact would be uneven across countries and sectors. The transition is also exposed to risks, including energy supply volatility. At the same time, it is rich in opportunity. The transition would prevent the buildup of physical climate risks and reduce the odds of initiating the most catastrophic impacts of climate change. Capital investment worth 1.5% of global GDP is required to finance the transition to NZE2050, according to the Energy Transitions Commission. A large new capital market must emerge, in which investments to decarbonize the global energy system are driven by the buying and selling of equity and debt instruments. The process of shifting global financial flows has begun. More than US$4 trillion was invested in so-called green bonds as of October 2023, according to the Climate Bonds Initiative.

Lithium: The rush is on for Africa’s “white gold”

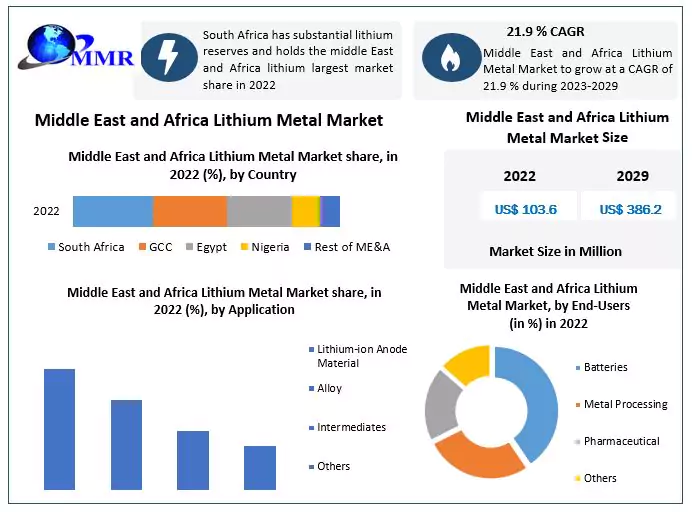

Sub-Saharan Africa is already at the center of global critical mineral production. In the global mining sector, African countries belong to economic blocks or cartel-like associations called ACP countries. Each country or region has reasons why these minerals are classified as critical. For most western countries, minerals are critical if they are essential for a low-carbon economy or for national security, have no substitutes, and are vulnerable to supply chain disruption. The Democratic Republic of Congo (DRC) accounts for over 70 percent of global cobalt output and approximately half the world’s proven reserves. South Africa, Gabon, and Ghana collectively account for over 60 percent of global manganese production. Zimbabwe, alongside the DRC and Mali, holds substantial but yet-to-be-explored lithium deposits. Other countries with significant critical mineral reserves include Guinea, Mozambique, South Africa, and Zambia. Lithium is a valuable mineral with multiple uses in the emerging green economy. Pure lithium is a soft, silvery-white metal. Lithium occurs naturally in felsic igneous rocks in the form of other lithium-rich mica (Lepidolite) or as a silicate mineral in pegmatites (Spodumene). Lithium in a refined form is used in the cathodes of lithium-ion battery (LIB) cells. Since 2010, the use of lithium for automotive-grade LIBs for electric vehicles has dominated global growth in the demand for lithium. With about 5% of the world’s lithium ore reserves, Africa still holds enormous potential, most of which is untapped. Currently, only Zimbabwe and Namibia export lithium ore, while projects in nations such as the Congo, Mali, Ghana, Nigeria, Rwanda, and Ethiopia are under exploration or development. These lithium-rich African countries aspire to increase the size of their processing and refining industries to earn a greater portion of the profits from the global expansion in demand for battery materials. Lithium-ion batteries are used in mobile phones, computers, electronics, energy storage systems, and electric vehicles. The forecast is that they will dominate the lithium market over the next few decades. However, there are many different types of lithium-ion batteries for different applications.

Africa’s primary contribution to lithium supply chains is likely to come via the mining of its extensive resources. As many companies develop lithium exploration and mining projects across Africa, offtake agreements are being signed, chiefly for the export of mineral concentrate to China. Global transportation of concentrate potentially represents a missed economic opportunity for the producing country and is also likely to have significant environmental impacts. The world’s lithium supply is currently dominated by Australia, Chile, and China, which together accounted for over 90% of the 130,000 metric tons produced globally in 2022. However, analysts note that with demand for lithium projected to increase sixfold between 2022 and 2035 if existing climate targets are to be reached, the landscape is set to change rapidly. Exploration-stage projects are gathering pace across the globe, and Africa is no exception. Lithium resources have been identified in Zimbabwe, Namibia, Ghana, the DRC, Mali, and Ethiopia. Several projects on the continent have been backed by major players in the battery and commodity industries, such as CATL, Ganfeng Lithium, and Glencore. Nevertheless, the vast majority of African lithium projects remain in the exploration or development stage. However, dominated by Chinese companies, the new lithium plants in Zimbabwe, along with many more in the pipeline in Mali, Ethiopia, the DRC, and Namibia, will almost treble the output of mined lithium from Africa in 2024 compared with last year, according to analysts. Unfortunately, African countries like Namibia, Zimbabwe, the DRC, and Ghana lack robust strategies for managing their critical mineral sectors, often being drawn into the global rush without proper frameworks. Furthermore, the quest for lithium is gaining traction in Nigeria, with competition becoming increasingly fierce. Namibia has banned the export of unprocessed lithium and other critical minerals in a move to profit from the energy transition by processing more minerals in the country.

Moving Beyond the Crossroads

An inclusive green economy is an alternative to today’s dominant economic model, which generates widespread environmental and health risks, encourages wasteful consumption and production, drives ecological and resource scarcity, and results in inequality. It is an opportunity to advance both sustainability and social equity as functions of a stable and prosperous financial system within the contours of a finite and fragile planet. Importantly, there is also an emerging practice in the design and implementation of national green economy strategies by both developed and developing countries across most regions, including Africa, Latin America, the Asia-Pacific, and Europe.

Linkages between the mining sector and other sectors give room for technology-based companies in other related sectors to enjoy agglomeration economies and hire the required human capital for their operations in African countries. In 2020, the transport sector accounted for 7.2Gt of CO2 emissions, equivalent to more than 20% of the global total. Electric road vehicles play a critical role in the greening of global transport, and the market has grown rapidly in recent years. Modernizing energy and industrial systems to drive energy transitions requires very large investments and the transformation of huge markets. It also comes with many significant benefits beyond mitigating climate change and reducing air pollution alone; in 2023, 36 million workers were employed across clean energy supply chains. An increased supply of lithium will be needed to meet the expected demand growth for lithium-ion batteries for transportation and energy storage. Lithium demand has tripled since 2017 and is set to grow tenfold by 2050 under the International Energy Agency’s (IEA) Net Zero Emissions by 2050 Scenario.

Transitioning to a green economy is an inevitable end game for all countries, and many have already started their journey. For those who have not, starting the process now is critical. Risk avoidance, compliance, and costs continue to be key drivers of green investments. The macroeconomics of this clean energy transition are highly uncertain. Economists need to be honest about the fact that solving the problem of climate change will be expensive, it will require fundamental shifts in the structure of the global economy, and it carries the risk of a negative supply shock as carbon-intensive capital is scrapped. At the same time, it also presents major opportunities for companies, investors, and governments. Hence, the green economy transition will play out differently depending on each country’s unique context. This is particularly true for emerging markets, which face their own set of challenges. Highly vulnerable to climate change, often fossil-fuel dependent, and financially constrained—these are just a few of the realities that emerging markets are facing in the transition.

If Africa wants to reap the rewards from its lithium industry, it must step up its game and learn to tame the dragon. An analyst says Africa needs stronger governance: regulations, accountability, and transparency. Mining policies and regulations must reflect the opportunities and challenges of meeting global demand for critical minerals. Mining companies operating in African countries should adhere to leading mining practices and national regulations to minimize the environmental and social impacts of their operations. The dynamics of governance and the political landscape in several African countries can frustrate potential gains that can be realized from resource-based industrialization and medium- and high-technology manufacturing. Countries should develop institutions such as pension funds, hedge funds, insurance, and wealth management institutions capable of pooling resources for significant investments like a mining operation. Developing local processing industries could significantly boost value added, create higher-skilled jobs, and increase tax revenues—thereby also supporting poverty reduction and sustainable development.

ـــــــــــــــــــــــــــــ

This article expresses the views and opinions of the author and does not necessarily reflect the views of Qiraat Africa and its editors.

{kind=link}